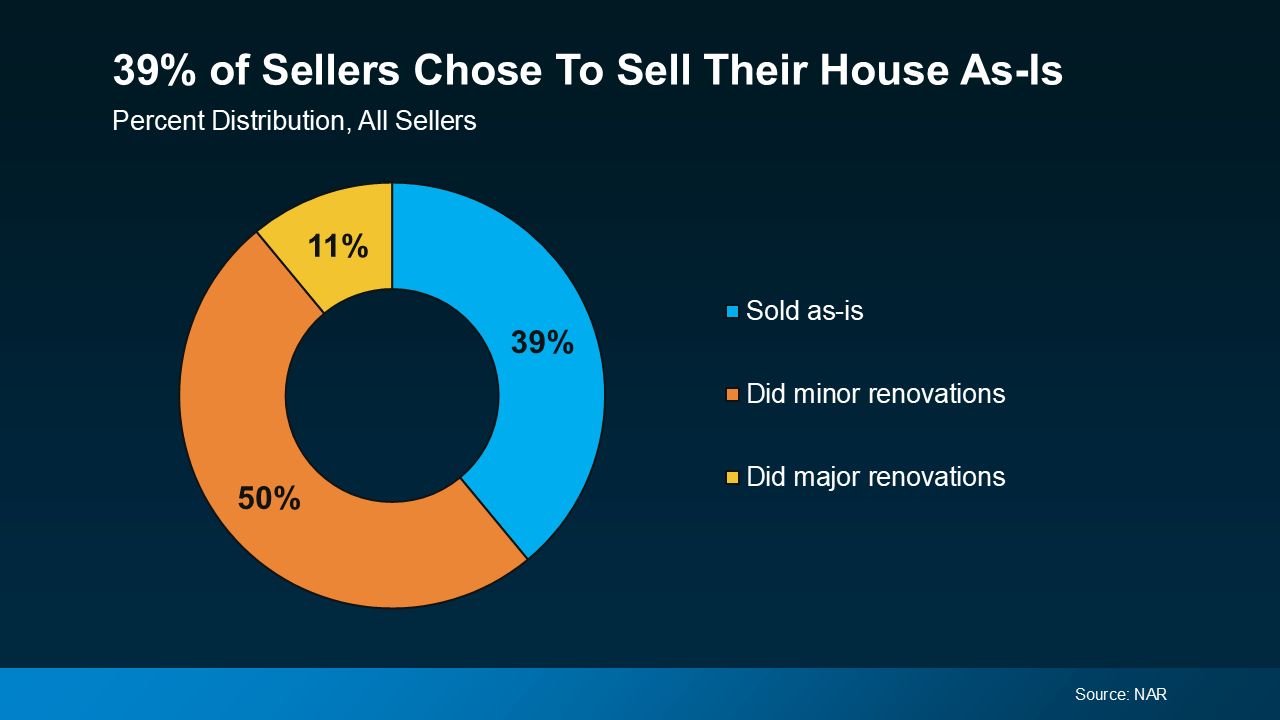

A recent study from the National Association of Realtors (NAR) shows most sellers (61%) completed at least minor repairs when selling their house. But sometimes life gets in the way and that’s just not possible. Maybe that’s why, 39% of sellers chose to sell as-is instead (see chart below):

If you’re feeling stressed because you don’t have the time, budget, or resources to tackle any repairs or updates, you may be tempted to sell your house as-is, too. But before you decide to go this route, here’s what you need to know.

If you’re feeling stressed because you don’t have the time, budget, or resources to tackle any repairs or updates, you may be tempted to sell your house as-is, too. But before you decide to go this route, here’s what you need to know.

What Does Selling As-Is Really Mean?

Selling as-is means you won’t make any repairs before the sale, and you won’t negotiate fixes after a buyer’s inspection. And this sends a signal to potential buyers that what they see is what they get.

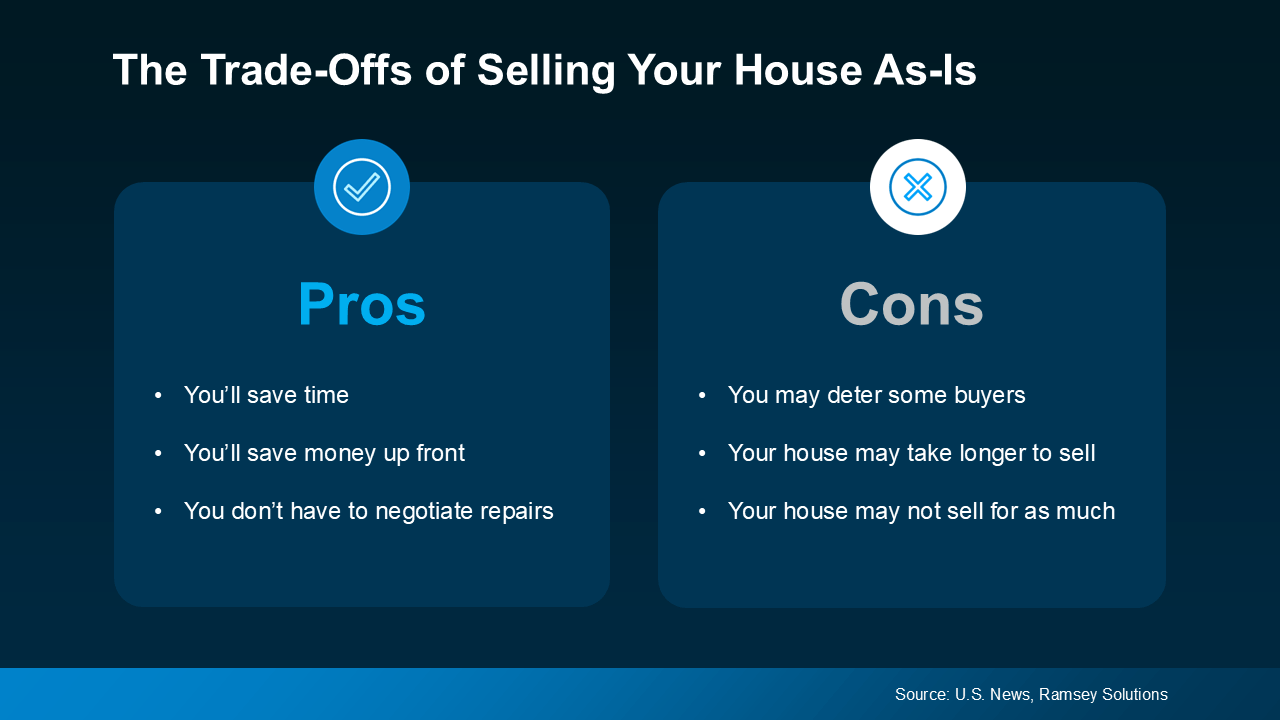

If you’re eager to sell but money or time is tight, this can be a relief because it’s that much less you'll have to worry about. But there are a few trade-offs you’ll have to be willing to make. This visual breaks down some of the pros and cons:

Typically, a home that’s updated sells for more because buyers are often willing to pay a premium for something that’s move-in ready. That’s why you may find not as many buyers will look at your house if you sell it in its current condition. And less interest from buyers could mean fewer offers, taking longer to sell, and ultimately, a lower price. Basically, while it’s easier for you, the final sale price might be less than you’d get if you invested in repairs and upgrades.

Typically, a home that’s updated sells for more because buyers are often willing to pay a premium for something that’s move-in ready. That’s why you may find not as many buyers will look at your house if you sell it in its current condition. And less interest from buyers could mean fewer offers, taking longer to sell, and ultimately, a lower price. Basically, while it’s easier for you, the final sale price might be less than you’d get if you invested in repairs and upgrades.

That doesn’t mean your house won’t sell – it just means it may not sell for as much as it would in top condition.

Here’s the good news though. In today’s market, as many as 56% of buyers surveyed would be willing to buy a home that needs some work. That’s because affordability is still a challenge, and while there are more homes for sale right now, inventory is lower than the norm. So, you might find there are a few more buyers who may be willing to take on the work themselves.

How an Agent Can Help

So, how do you make sure you’re making the right decision for your move? The key is working with a pro.

A good agent will help you weigh your options by showing you what comparable homes in your area have sold for, what updates your neighbors are making, and guide you in setting a fair price no matter what you decide. That helps you anticipate what your house may sell for either way – and that can be a key factor in your final decision.

Once you’ve picked which route you’re going to go and the asking price is set, your agent will market your house to maximize its appeal. And if you decide to sell as-is, they’ll call attention to the best features, like the location, size, and more, so it’s easy for buyers to see the potential, not just projects.

Bottom Line

Selling a home without making any repairs is possible in today’s market, but it does have some trade-offs. To make sure you’re considering all your options and making the best choice possible, have a conversation with a local agent.